Chapter 2.1 - Internet Transit Prices - Historical and Prospective

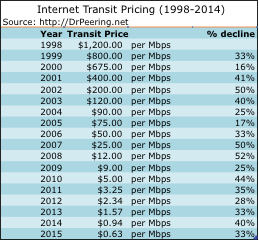

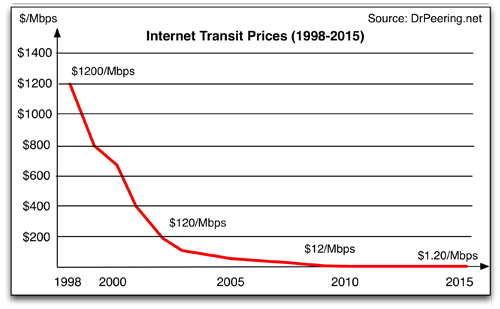

I have been tracking the price of Internet Transit since 1998, and as you can see from Table 2-2 and Figure 2-4, the prices for Internet Transit have dropped every year.

Table 2-2. U.S. Internet Transit Prices (1998–2014) Historical and Projected

It is worth pointing out that these data have always generated heated debate in the peering coordinator community.

Internet Transit May Have SLAs

Service-Level Agreements (SLAs) are contracts with financial penalties for failure to meet specified service levels. They are intended to punish an ISP for failure to meet the explicit customer expectations. Many Internet Transit customers I have spoken with have said that they felt comforted by these financial penalties, these “teeth.”

Internet Transit SLAs, however, are widely dismissed by the network operators as merely insurance policies. The ISPs I spoke with said that it is common practice to simply price the Internet Transit service higher when it includes SLAs, and with the increased pricing proportional to the likelihood of their failure to meet the SLA requirements. Further, the customer has to notice the SLA failure, file for the SLA credits, and check to see that credits are indeed applied. Some ISPs see SLAs as a way to simply increase margins without needing to improve the service.

Notes from the field.

Internet Transit Pricing Data and Controversy

The controversy over these numbers is related to the variability in service offerings and pricing. Further, the pricing schedules are often protected under a nondisclosure agreement (NDA), and generally not publicly available to systematically analyze. Some ISPs consider many variables when determining pricing. They might, for example, account for the number and size of the ports requested, type of the customer traffic (inbound vs. outbound), how that traffic would impact the ISP, the region(s) and market conditions at the location of the interconnection, etc. For these reasons, many would argue that there is no single market price for Internet Transit. The data are inherently flawed.

And they have a valid point.

My data are anecdotal and based on a variable and small sample size, polling maybe 30–50 people three to five times a year. The transit price points are collected on an ad-hoc basis at operations conferences that I attend every year. I ask ISPs and transit customers, "What is the going price for transit these days?” From the dataset I throw out the outliers and select the middle from the mass of numbers that fall within a narrow range.

However flawed this manual measurement system is, it remains one of the very few longitudinal measures of the market price for transit. Some of these measurements were based on or validated by contributed ISP pricing sheets. One can say "according to the conversations Bill has had with ISPs over the years, the transit prices have dropped roughly like this line." I would not recommend taking these numbers as anything but very rough indications—and a better mechanism is on its way as we start measuring in $/Gbps.

Besides, to focus on the individual data points is to miss the point.

The point is that the trend is unmistakable, and no one would disagree—because transit prices have dropped every year.

The other interesting thing I noticed is that every year the ISPs say to me things like, “Transit prices can’t get any lower,” and “No one is making any money at these prices.” And every year, the prices drop again.

The other interesting thing I noticed is that every year the ISPs say to me things like, “Transit prices can’t get any lower,” and “No one is making any money at these prices.” And every year, the prices drop again.

Figure 2-4. Internet Transit prices historically decline every year.

The good news for ISPs is that Internet traffic volumes have always grown as well, and all indications are that this trend will continue for some time. Even though the price of transit has declined by around 30% per year, Internet traffic typically increases by more than 50% per year.

Variability in Internet Transit Service

There is also some debate within the community on the qualitative differences between transit from a lower-priced provider and the Internet transit service delivered from a higher-priced provider. Higher-priced providers would argue that they have better-quality equipment (routers vs. switches, etc.), and better and more sustainable operations procedures that simply cost more to operate. They would argue that “you get what you pay for in the transit market”. They could be right, but I would also point out that I have not met very many paying customers complaining about the quality of service of lower-priced providers.

Internet Transit is a Customer-Supplier Relationship

Some content providers prefer a transit service (paying customer) relationship with ISPs for business reasons. They argue that they will get better service with a paid relationship than with any free or “special deal”, bartered, or “peering” relationship.

Implementation Model for the Internet Transit Service

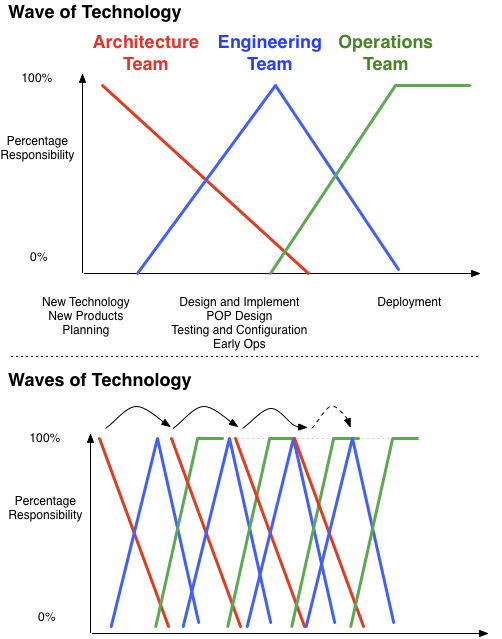

While a complete exploration of the ISP business models is beyond the scope of this book, a few commonalities across ISPs are worth highlighting. Every year the underlying technologies get better, cheaper, and faster. These advancements tend to come in waves. As a result, most larger ISPs have an Architecture-Engineering-Operations workflow, with responsibilities being transitioned between these disciplines as shown in Figure 2-5.

Observations about Internet Transit

To finish this chapter, let’s highlight a few important characteristics about Internet Transit:

- Internet Transit is a simple service from the customer perspective. All you need to do is pay for the Internet Transit service, and all traffic sent to the upstream ISP is delivered to the Internet.

- Internet Transit is typically a metered service. The more you send or receive, the more you pay.

- Internet Transit has commits and discounts. Upstream ISPs often provide volume discounts based on negotiated commit levels. Thus, if you commit to 10Gbps of transit per month, you will likely get a better unit price than if you commit to only 1Gbps of transit per month. However, you must pay for (at least) the commit level worth of transit regardless of how much traffic you send.

- Internet Transit contracts have a term, a duration.

- Internet Transit prices drop every year.

That is what you need to know about Internet Transit. In the next chapter we will discuss the "tricks of the trade" that some have used in an attempt to improve the efficiency of their transit service purchase.

Figure 2-5 The Architecture-Engineering-Operations new technology waves and responsibilities.

When new technologies are considered for a network, the ISP Architecture team evaluates the applicability and designs a solution. Once accepted, the solution moves through a joint Architecture/Engineering development phase, during which the Engineering team increasingly takes over responsibility for the deployment of the technology. The Operations group takes over responsibility from the engineering team as the technology hardens and the logistical transition challenges are worked through. The Engineering team eventually is removed from the day-to-day operations activities of the technology, and the Operations team runs the technology in the production network.

This cycle continues as the next wave of technology becomes available and the Architecture team looks at its applicability. These technology waves apply to backbone infrastructure (routers, transmission gear) as well as edge devices (routers, switches, auxiliary services) and support systems.

These waves of technology are important because they enable the ISPs to compete more effectively in the Internet Transit market. Those with old equipment simply can't compete with the economies of scale realized by the large players.

Peering Workshop Discussions

Here are a few discussion questions from the Internet Peering Workshop.

1. I am purchasing Internet Transit from ISP A for $5 per Mbps with no commits. At the end of the month I send 500Mbps and receive 800Mbps at the 95th percentile. What is my monthly bill?

A) $5/month B) $2500/month C) $4000/month D) $6500/month

2. I am purchasing Internet Transit from ISP B for $5 per Mbps but I am considering buying its 1Gbps commit transit product at a price of $3/Mbps. I still expect to send 500Mbps and receive 800Mbps at the 95th percentile. Should I commit to 1Gbps?

Answers to these questions along with related FAQs and supplemental materials are here:

http://DrPeering.net/books/The-Internet-Peering-Playbook/transit.php